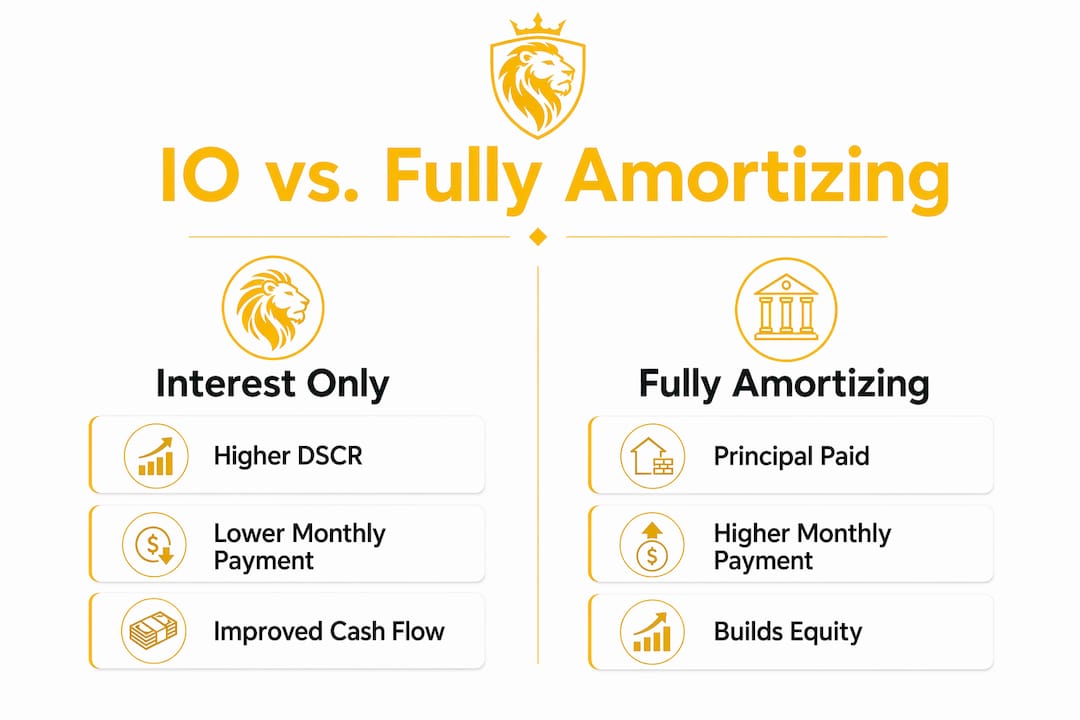

An interest only DSCR loan is defined as a real estate financing product where the borrower pays only interest during an initial period, reducing monthly obligations and improving the property's Debt Service Coverage Ratio. DSCR qualification is based solely on rental income divided by monthly debt obligations, including principal, interest, taxes, insurance, and association dues (PITIA). During the interest only period, the principal portion drops to zero, which directly lowers the denominator in the DSCR formula and raises the ratio. This structure gives investors a measurable cash flow advantage without requiring a change in rental income. Interest only periods typically run 5, 7, or 10 years on 30 or 40 year loan terms, making them a flexible tool for a wide range of investment strategies.

How do interest only periods impact DSCR calculations and cash flow?

The DSCR formula compares gross rental income to total monthly debt service. With a standard fully amortizing loan, that debt service includes both principal and interest, taxes, insurance, and any HOA dues (PITIA). With an interest only structure, the calculation shifts to ITIA: interest, taxes, insurance, and association dues only. Removing the principal component directly reduces the monthly payment, which raises the DSCR ratio.

Interest only DSCR loans increase the DSCR ratio by 0.13 to 0.15 points compared to a fully amortizing loan on the same property. That improvement frequently separates a deal that fails to qualify at a sub-1.0x DSCR from one that clears the lender's minimum threshold. For investors working with properties in competitive markets where rent-to-price ratios are tight, this distinction is often the difference between closing and walking away.

The table below illustrates the practical effect on a $400,000 loan at a 7.5% rate with $2,200 in monthly rent, $400 in taxes and insurance combined:

| Structure | Monthly Payment | DSCR Ratio |

|---|---|---|

| 30-year fully amortizing | $2,797 | 0.79x |

| Interest only (IO period) | $2,500 | 0.88x |

| 40-year fully amortizing | $2,660 | 0.83x |

The IO structure produces the highest DSCR in every scenario. Investors can use the DSCR calculator from Jakenfinancegroup to model these numbers against their specific property and market before committing to a loan structure.

Pro Tip: Run both the IO and fully amortizing DSCR scenarios side by side before applying. A 0.13 point DSCR lift sounds small but can determine whether a lender approves or declines your deal.

What are the loan terms, qualifications, and costs?

Interest only periods typically last 5, 7, or 10 years, after which the loan recasts to a fully amortized schedule over the remaining term. These products are widely available for 1–4 unit residential properties and select 5–10 unit multifamily assets in 2026. The overall loan term is usually 30 or 40 years, giving investors a long runway even after the IO period ends.

Qualification standards for interest only DSCR loans are stricter than for standard DSCR products. Lenders require stronger borrower profiles because the IO structure carries higher perceived risk. Specifically, investors should expect:

- Minimum DSCR: 1.0x to 1.25x during the IO period, calculated on ITIA payments

- Credit score: Higher FICO scores required compared to standard DSCR loans; many lenders set minimums at 680 or above

- Down payment: Typically 20%–25% of the purchase price, supporting loan to value DSCR ratios at 75%–80% LTV

- Cash reserves: Lenders require documented reserves, often 6–12 months of PITIA payments

- Rate premium: Investors pay 0.125% to 0.375% above standard DSCR loan rates for the IO feature

- Underwriting scrutiny: More documentation and review compared to standard DSCR loans

The rate premium reflects the lender's added risk during the IO period, when no principal reduction occurs. That cost is real but often justified by the cash flow improvement the IO structure delivers. Mortgage experts note that IO loans facilitate qualifying at higher LTV ratios of 80%–85% for borrowers who meet the stronger credit and reserve requirements.

Pro Tip: Build your cash reserve documentation before applying. Lenders scrutinize reserves heavily on IO loans. Showing 12 months of PITIA in liquid accounts strengthens your file significantly.

What are the risks of an interest only DSCR loan?

The most significant risk in an interest only DSCR loan is payment shock. When the IO period ends, the loan recasts to a fully amortizing schedule over the remaining term. Because years of principal payments were skipped, the remaining balance amortizes over a shorter period, which sharply increases monthly payments.

Payment shock after the IO period ends can increase monthly payments by 25% to 55%. A payment that was $2,500 per month during the IO period could jump to $3,125–$3,875 once principal amortization begins. If rental income has not grown proportionally, the property's DSCR can fall below the lender's minimum, creating refinance pressure or cash flow shortfalls.

Investors should address this risk with a clear exit or refinance plan before closing. The steps below create a practical framework:

- Model the recast payment before closing. Calculate the fully amortized payment on the remaining balance and remaining term. Confirm the property's projected rent covers that payment at a 1.0x DSCR or better.

- Plan refinancing 12–18 months before IO expiration. Refinancing strategies can extend the IO period, reset the loan term, or transition to a fully amortizing structure depending on market conditions at that time.

- Account for prepayment penalties. Many DSCR loans carry prepayment penalties of 3–5 years. Refinancing before the penalty period expires adds cost to the exit strategy.

- Project rental income growth. If rents in the target market grow at a consistent rate, the recast payment may be covered by higher income at IO expiration. Model conservative and optimistic rent scenarios.

- Identify market conditions for refinance success. Rate environments and property values at the time of refinance determine whether a new loan improves or worsens the investor's position.

"The IO period is not free money. Every month of interest only payments is a month where the loan balance stays flat. Investors who treat IO loans as a long term solution without a refinance or exit plan often face a difficult choice when the recast hits: sell at a loss, refinance at a worse rate, or absorb a payment increase that kills cash flow."

How can investors use interest only DSCR loans strategically?

Interest only DSCR loans align well with investors seeking rapid portfolio scaling, value add projects, or defined exit timelines within 5–10 years. The key is matching the IO period length to the investment strategy rather than selecting IO simply to qualify.

Different IO period lengths serve different investor profiles:

- 5-year IO period: Best for investors with a defined exit within 5 years, such as a fix and rent strategy with a planned sale or refinance. The shorter IO window keeps the rate premium lower and aligns with shorter hold periods.

- 7-year IO period: Suited for investors who need cash flow relief during a stabilization or lease-up phase. Seven years provides enough runway to increase rents and property value before the recast.

- 10-year IO period: Appropriate for long term hold investors who want maximum cash flow during the first decade. This structure works well in markets with strong rent growth trajectories.

Investors scaling a portfolio benefit from IO loans because lower monthly payments free capital for additional acquisitions. A fully amortizing loan on a $400,000 property might require $300 more per month in debt service than an IO loan. Across five properties, that difference represents $1,500 per month in retained capital available for reserves, repairs, or down payments on new acquisitions.

Comparing IO loans to fixed rate and ARM DSCR loan options reveals clear trade-offs. Fixed rate fully amortizing loans build equity steadily and carry no payment shock risk. ARM DSCR loans offer lower initial rates but introduce rate risk after the adjustment period. IO loans deliver the highest initial cash flow but require active management of the IO expiration event. The right structure depends on the investor's hold period, risk tolerance, and refinance capacity.

Pro Tip: Always model both the IO and fully amortizing payment structures side by side using current market rates. The IO structure wins on cash flow during the IO period, but the fully amortizing structure wins on equity accumulation. Know which metric matters more for your specific deal before choosing.

For investors evaluating markets, the cash flow analysis across Charlotte, Raleigh, and Atlanta shows how IO structures perform differently depending on local rent levels and property prices.

Key Takeaways

Interest only DSCR loans deliver measurable cash flow advantages during the IO period, but require disciplined exit planning to avoid payment shock when the loan recasts.

| Point | Details |

|---|---|

| DSCR lift from IO structure | IO loans raise DSCR by 0.13–0.15 points by removing principal from monthly payment calculations. |

| IO period lengths | Common IO periods are 5, 7, and 10 years on 30 or 40 year loan terms. |

| Rate premium cost | Investors pay 0.125%–0.375% above standard DSCR rates for the interest only feature. |

| Payment shock risk | Monthly payments can increase 25%–55% when the IO period ends and principal amortization begins. |

| Refinance planning | Begin refinance planning 12–18 months before IO expiration to avoid being forced into unfavorable terms. |

What I have learned from watching investors use IO DSCR loans

The investors who use IO DSCR loans well are not the ones chasing the lowest monthly payment. They are the ones who treat the IO period as a defined window with a specific purpose: scale faster, stabilize a property, or preserve capital for a value add project. The IO period is a tool, not a strategy by itself.

The mistake I see most often is investors who select a 10 year IO period because it produces the best DSCR at closing, without modeling what the recast payment looks like in year 11. They close the deal, collect rent for a decade, and then face a payment increase that their rental income cannot absorb. At that point, their options narrow fast.

The rate premium of 0.125%–0.375% is genuinely small compared to the cash flow benefit in most deals. Where investors get into trouble is treating that premium as the only cost. The real cost is the equity they did not build during the IO period. If property values drop or rates rise at IO expiration, refinancing becomes expensive or impossible. That is when the IO loan stops looking like a good trade.

My recommendation: work with a lender who will show you the recast payment before you sign, not after. Any lender worth working with runs that number upfront. If they do not, ask for it directly.

— Jason

Financing options for real estate investors at Jakenfinancegroup

Real estate investors who want to put IO DSCR loan structures to work need a lender who understands asset based financing and moves at investment speed.

Jakenfinancegroup offers DSCR loan programs for 1–4 unit residential and multifamily properties, including interest only structures designed to improve cash flow and qualification ratios. The team at Jakenfinancegroup specializes in financing for investors across the United States, with a focus on speed, flexibility, and deal structure. For investors who need hard money or bridge financing before transitioning to a DSCR product, Jakenfinancegroup provides hard money loan solutions built for that exact sequence. Contact Jakenfinancegroup directly to discuss IO DSCR loan options for your next acquisition.

FAQ

What is an interest only DSCR loan?

An interest only DSCR loan is a rental property loan where the borrower pays only interest during an initial period of 5, 7, or 10 years, reducing monthly payments and improving the property's Debt Service Coverage Ratio. DSCR qualification is based on rental income divided by monthly debt obligations, and removing the principal component raises that ratio by 0.13–0.15 points.

How do I qualify for an interest only DSCR loan?

Qualifying requires a DSCR of 1.0x to 1.25x during the IO period, a higher FICO score than standard DSCR loans, a down payment of 20%–25%, and documented cash reserves of 6–12 months of PITIA payments. Lenders apply stronger underwriting standards because the IO structure carries higher perceived risk.

What is the rate premium for an interest only DSCR loan?

Investors pay a rate premium of 0.125%–0.375% above standard DSCR loan rates for the interest only feature. That premium reflects the lender's added risk during the IO period when no principal reduction occurs on the loan balance.

What happens when the interest only period ends?

The loan recasts to a fully amortizing schedule over the remaining term, which can increase monthly payments by 25%–55%. Investors should model the recast payment before closing and begin refinance planning 12–18 months before IO expiration to avoid being forced into unfavorable terms.

Which investors benefit most from interest only DSCR loans?

Investors with defined exit timelines of 5–10 years, those pursuing value add projects, and investors scaling a portfolio quickly benefit most from IO DSCR structures. Matching the IO period length to the specific hold strategy is the key factor in using these loans effectively.